Introduction

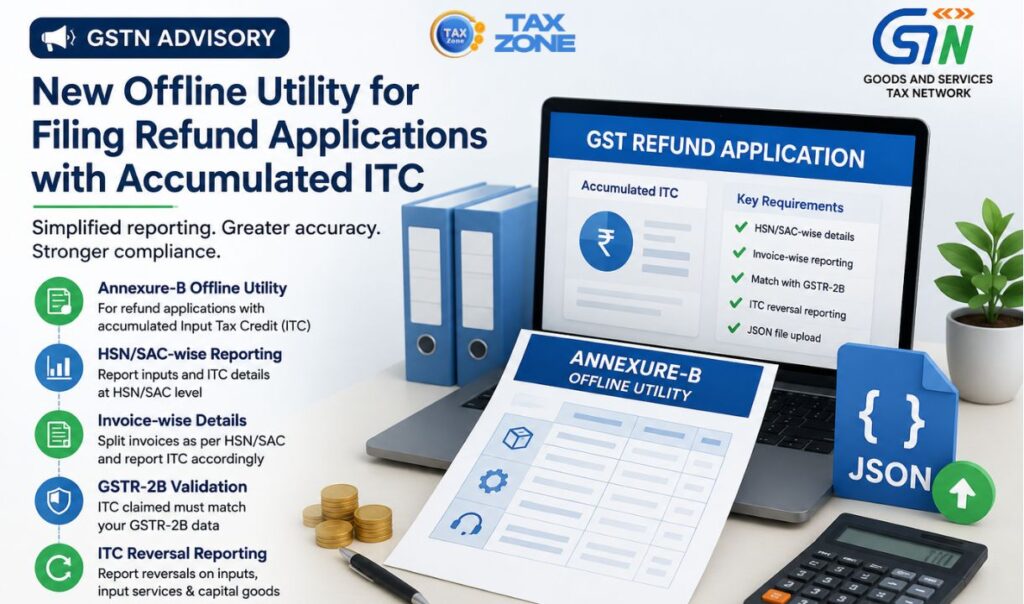

The Goods and Services Tax Network (GSTN) has introduced a major procedural change in the refund filing process (GST Refund Advisory 2026) for taxpayers claiming refunds involving accumulated Input Tax Credit (ITC). Through an advisory dated 18 May 2026, GSTN announced that taxpayers will now be required to file Annexure-B using a standardized Offline Utility instead of uploading Annexure-B in PDF format.

This change is extremely important for exporters, SEZ suppliers, and businesses claiming refunds due to the inverted tax structure because it completely changes the method of reporting inward supply invoices for refund applications.

Earlier, taxpayers were manually preparing Annexure-B in PDF format and uploading it with refund applications in Form GST RFD-01. However, the new system introduces invoice-level reporting through an Excel-based offline utility along with JSON upload functionality. The purpose of this new mechanism is to automate verification, improve accuracy, reduce manual intervention, and enable system-based validation with GSTR-2B.

Many taxpayers may initially find this new process confusing because the advisory contains technical instructions related to HSN/SAC-wise reporting, invoice splitting, validation rules, ITC reversals, and JSON uploads. Therefore, this article explains the advisory in a simple and practical manner so that taxpayers, accountants, consultants, exporters, and finance professionals can easily understand the new refund filing requirements.

Background of Annexure-B in GST Refunds

Under the GST law, certain taxpayers are eligible to claim a refund of accumulated ITC. This usually happens in situations where:

- Exports are made without payment of tax under LUT/Bond.

- Supplies are made to SEZ units or developers without payment of tax.

- Input tax rate is higher than the output tax rate, resulting in an inverted duty structure.

- Export of electricity is made without payment of tax.

While filing such refund applications, taxpayers are required to provide details of inward supplies on which ITC has been claimed.

Traditionally, these details were submitted through Annexure B in PDF format. Since the format was not standardized, different taxpayers prepared Annexure-B differently. This created difficulties for:

- Departmental verification

- Matching invoices with GSTR-2B

- Identifying duplicate claims

- Verifying ITC reversals

- Processing refunds efficiently

To solve these problems, GSTN has now introduced a structured and automated Annexure-B Offline Utility.

Objective Behind Introducing the Annexure-B Offline Utility

The primary objectives of introducing the new utility are:

- Standardization of Data-All taxpayers will now furnish refund-related inward supply details in a uniform format.

- Automation of Verification-The GST system will automatically validate invoices with GSTR-2B data.

- Reduction in Manual Scrutiny- Proper invoice-wise reporting will reduce dependency on manual examination by officers.

- Faster Refund Processing- Since invoice data will already be system-validated, refund processing may become quicker.

- Prevention of Errors and Duplicate Claims-The utility includes validation checks to identify duplicate invoice entries and incorrect reporting.

- Better Transparency-Taxpayers will be able to identify invalid invoices before filing the refund application.

Refund Categories Covered Under the New Utility

The new Annexure-B Offline Utility is mandatory for the following refund categories:

- Export of Goods or Services Without Payment of Tax-This includes exporters who export under LUT/Bond and claim a refund of unutilized ITC. However, the export of electricity has been separately classified.

- Supplies to SEZ Unit or SEZ Developer Without Payment of Tax-Businesses supplying goods or services to SEZ entities without payment of tax while claiming refund of accumulated ITC are also required to use the utility.

- Refund Due to Inverted Tax Structure-Where the rate of tax on inputs is higher than the rate of tax on outward supplies, accumulated ITC may arise. Refund claims under Section 54(3) due to inverted duty structure are covered.

- Export of Electricity Without Payment of Tax-Electricity exporters claiming refund of accumulated ITC are also included.

What is the Annexure-B Offline Utility?

The Annexure-B Offline Utility is an Excel-based tool provided on the GST portal. Taxpayers are required to:

- Download the utility.

- Enter the inward supply invoice details.

- Validate the data.

- Generate a JSON file.

- Upload the JSON file while filing RFD-01.

This utility replaces the earlier PDF-based Annexure-B filing method.

Major Structural Changes Introduced in the New Utility

The advisory introduces several important reporting changes. Taxpayers must understand these carefully.

HSN/SAC-Wise Reporting is Now Mandatory

One of the most important changes is that invoice details must now be reported HSN/SAC-wise. Earlier, taxpayers often reported invoice values in consolidated form. Under the new system, invoice details must be split based on:

- HSN/SAC code

- Type of supply

- Category of ITC

This means each line item in the utility should correspond to:

- One HSN/SAC code

- One category of input supply

Categories of Input Supply

The advisory specifically mentions three categories:

- Inputs: Raw materials and goods used in business.

- Input Services: Services used in business operations.

- Capital Goods: Assets such as machinery, equipment, etc.

If a single invoice contains all three categories, the invoice must be split into separate line items.

Understanding Invoice Splitting with Example

Suppose a taxpayer receives one invoice from a supplier containing:

- Raw material worth Rs. 1,00,000

- Professional service worth Rs. 20,000

- Machinery worth Rs. 80,000

Further, assume different HSN/SAC codes apply.

Under the new utility:

- The invoice cannot be reported in one consolidated row.

- Separate rows must be created for:

- Inputs

- Input services

- Capital goods

- Separate HSN/SAC-wise breakup must also be provided.

Thus, a single invoice may result in multiple entries in Annexure-B. This is one of the biggest practical changes introduced by GSTN.

Distribution of Invoice Value and Tax Amount

Where invoices are split into multiple line items, taxpayers must proportionately distribute:

- Taxable value

- IGST

- CGST

- SGST

- Cess

Incorrect distribution may lead to:

- Validation failure

- Mismatch with GSTR-2B

- Rejection of refund claim

- Queries from the department

Therefore, taxpayers should maintain proper working papers for invoice bifurcation.

Maximum Number of Entries Allowed

GSTN has imposed the following limits:

- Per Utility File- Maximum 10,000 line items can be entered in one utility file.

- Per Refund Application- Maximum 25 utility files can be uploaded.

Thus, the total limit per refund application is: 2,50,000 line items.This limit is particularly important for:

- Large exporters

- E-commerce businesses

- Manufacturing companies

- Businesses with a huge vendor base

What if Line Items Exceed 2,50,000?

If total line items exceed 2,50,000:

- Remaining invoices can be submitted as PDF supporting documents.

- Taxpayers should upload the maximum permissible line items through the utility.

GSTN has also clarified that higher-volume data handling functionality may be introduced in future updates.

Structure of the Annexure-B Utility

The utility contains two major tables.

Table 1 – Reversal Details-This table captures ITC reversals.

Table 2 – HSN/SAC-wise Inward Invoice Details-This table captures invoice-wise inward supply details for which ITC has been claimed in GSTR-3B.

Both tables are extremely important and should be filled carefully.

Reporting of ITC Reversals

The advisory places special emphasis on proper reporting of ITC reversals. Taxpayers must report reversals relating to:

- Rule 38

- Rule 42

- Rule 43

- Section 17(5)

Other reversals reported in Table 4(B)(2) of GSTR-3B

Importance of Correct Reversal Reporting

Incorrect reversal reporting may result in:

- Excess refund claim

- Notice from the department

- Refund rejection

- Interest and penalty exposure

Therefore, reversal figures should reconcile with:

- GSTR-3B

- Electronic Credit Ledger

- Books of accounts

Special Rule for Multiple Utility Files

If multiple utility files are uploaded:

- The reversal amount should be entered only in the final utility file.

- Earlier utility files should show the reversal amount as zero.

This is because the GST system consolidates all uploaded JSON files and recalculates Net ITC. Taxpayers must carefully verify the consolidated summary before final submission.

Duplicate Document Validation

GSTN has introduced strong duplicate validation controls.Validation will be applied separately for:

- Supplier GSTIN

- Invoice number

- Invoice date

- Category of input supply

- HSN/SAC

If all these parameters are identical, multiple entries will not be accepted.

Important Practical Point

Suppose:

- Same invoice number

- Same supplier

- Same HSN/SAC

- Same category

Then only one line item is allowed. However, if HSN/SAC differs or the category differs, separate line items are permitted. This distinction is very important while splitting invoices.

Upload Process of Annexure-B JSON File

After entering data in the utility:

- Validate data.

- Generate JSON file.

- Open refund application in RFD-01.

- Click “Click to upload the Statement of invoices (Unutilized ITC)” link.

- Upload JSON file.

- Proceed for system validation.

Only after successful upload and validation can the refund application proceed.

Validation with GSTR-2B

One of the most significant changes introduced through the advisory is validation with GSTR-2B. The GST system will compare uploaded invoice data with GSTR-2B.

Valid Documents Sheet

If the invoice matches with GSTR-2B:

- It will appear in the Valid Documents Sheet.

- The system will indicate whether invoice is present in GSTR-2B.

This feature will help taxpayers identify missing invoices before final submission.

Treatment of Old Invoices up to October 2024

GSTN has provided special relaxation for invoices relating to periods up to October 2024.For such invoices:

- System will not validate with GSTR-2B.

- Taxpayers can still upload such invoices.

- Generic message may appear stating invoice is not validated.

- This should not be treated as an error.

This clarification is extremely important because older GSTR-2B data may not be available in the validation system.

Invoices from November 2024 Onwards

For invoices relating to November 2024 or later:

- Full validation with GSTR-2B will apply.

- Mismatches will appear in Invalid Documents Report.

This means taxpayers should ensure:

- Supplier has filed GSTR-1 properly.

- Invoice appears in GSTR-2B.

- Invoice details are correctly entered.

Otherwise refund processing may face delays.

Common Reasons for Validation Failure

Some likely reasons include:

- Incorrect invoice number

- Wrong invoice date

- HSN/SAC mismatch

- GSTIN error

- Incorrect tax amount

- Duplicate invoice entry

- Supplier non-filing of GSTR-1

- ITC not reflected in GSTR-2B

- Additional spaces in fields

Taxpayers should reconcile data before upload.

Copy-Paste Functionality in Utility

GSTN has enabled copy-paste functionality in dropdown fields.However, taxpayers must ensure:

- Exact dropdown values are used.

- No extra spaces are inserted.

- Protected fields are not modified.

Even minor differences may cause validation errors.

Avoid Extra Spaces

The advisory repeatedly warns taxpayers against unnecessary spaces.

Examples:

- Extra spaces after the supplier name

- Leading spaces

- Trailing spaces

Such small mistakes may result in:

- JSON generation failure

- Upload issues

- Validation mismatch

This indicates that the utility is highly system-driven and sensitive to formatting inconsistencies.

Do Not Modify JSON File Directly

After generating JSON:

- Taxpayers should not edit the JSON manually.

- Any correction must be made in Excel utility.

- Fresh JSON should then be generated.

GSTN has also advised not to rename JSON file after creation. This is important because altering JSON structure may corrupt the file and cause upload failures.

Importance of Internal Data Preparation

The new system clearly indicates that refund filing under GST is becoming increasingly data-driven.Businesses should now maintain:

- Proper invoice classification

- HSN/SAC mapping

- Vendor reconciliation

- GSTR-2B matching

- ITC reversal tracking

Manual and unstructured data handling may create refund difficulties.

Impact on Exporters

Exporters are likely to experience the biggest impact.Why? Because exporters generally:

- Claim large refund amounts

- Have huge volume of inward invoices

- Deal with multiple vendors

- Use numerous HSN/SAC codes

The new utility will require significant invoice-level data management. However, once systems are streamlined, refund processing may become faster and more transparent.

Impact on Chartered Accountants and GST Consultants

GST professionals must now:

- Educate clients regarding utility usage

- Ensure reconciliation with GSTR-2B

- Review ITC reversals carefully

- Verify HSN/SAC classifications

- Check invoice splitting logic

Professional scrutiny before filing refund applications will become even more important.

Impact on ERP and Accounting Software

Businesses using ERP systems should consider:

- HSN-wise extraction capability

- Input category mapping

- Refund-specific reporting formats

- JSON-compatible data structure

Software customization may become necessary for smooth refund compliance.

Practical Compliance Tips for Taxpayers

- Start Preparing Data Early-Do not wait until the refund filing date.

- Reconcile with GSTR-2B Regularly- Monthly reconciliation will reduce refund issues.

- Maintain Proper HSN/SAC Mapping-Ensure every inward invoice is correctly classified.

- Review ITC Reversal Working-Reversal mismatches may create serious refund disputes.

- Validate Vendor Compliance-Ensure suppliers file GSTR-1 timely.

- Avoid Manual Errors-Double-check invoice numbers, dates, and tax amounts.

- Use Standard Naming Conventions-Consistent data entry helps avoid validation failures.

- Preserve Supporting Documents-Keep invoice copies and reconciliation workings ready for departmental verification.

Challenges Taxpayers May Face Initially

Although the new system is beneficial, taxpayers may face certain initial challenges.

- Increased Data Entry Burden-HSN/SAC-wise reporting significantly increases workload.

- Invoice Splitting Complexity-Businesses with mixed invoices may struggle.

- Validation Errors-Minor formatting mistakes may create issues.

- Software Compatibility-Existing accounting systems may not generate the required format.

- Large Volume Handling-Exporters with lakhs of invoices may face operational challenges.

However, over time, businesses are likely to adapt to the system.

Benefits of the New System

Despite challenges, the advisory introduces several long-term benefits.

- Better Transparency-Invoice-level validation improves clarity.

- Faster Refund Processing-Automated verification may reduce manual scrutiny.

- Reduced Fake Claims-Duplicate validations improve compliance.

- Improved Data Accuracy-Structured reporting minimizes inconsistencies.

- Stronger Audit Trail-Detailed invoice mapping strengthens documentation.

Important Points Taxpayers Should Remember

- Annexure-B PDF upload method is effectively replaced.

- Utility filing is mandatory for specified refund categories.

- HSN/SAC-wise reporting is compulsory.

- Invoice splitting may be required.

- Validation with GSTR-2B is system-driven.

- Duplicate invoices will not be accepted.

- Reversal reporting must match GSTR-3B.

- JSON should not be edited manually.

- Extra spaces may cause errors.

Old invoices up to October 2024 get relaxation from validation.

Conclusion

The GSTN advisory introducing the Annexure-B Offline Utility marks a significant shift toward technology-driven refund processing under GST.

The new system aims to create standardization, improve transparency, strengthen invoice verification, and accelerate refund processing through automated validations. Although taxpayers may initially face practical challenges due to invoice splitting, HSN/SAC-wise reporting, and GSTR-2B validation requirements, the system is expected to bring long-term efficiency and accuracy.

Businesses claiming refunds involving accumulated ITC must immediately upgrade their internal data management practices and reconciliation mechanisms. Exporters, SEZ suppliers, manufacturers under the inverted duty structure, and GST professionals should carefully understand the new reporting requirements to avoid refund delays, validation failures, and departmental objections.

The advisory clearly indicates that GST compliance is steadily moving toward detailed invoice-level digital verification. Therefore, businesses that maintain accurate records, perform timely reconciliations, and adopt structured compliance systems will be in a much stronger position for smooth refund processing in the future.

Taxpayers are strongly advised to carefully read the instructions provided in the utility, test the filing process in advance, and ensure proper coordination between accounts, tax, and ERP teams before filing refund applications using the new Annexure-B mechanism.

Related Post: