TDS on Payments to Residents – Income Tax Act 2025 Explained

The Income Tax Act, 2025 introduces a structured and simplified framework for Tax Deducted at Source (TDS) on various payments made to residents. Earlier, TDS provisions were scattered across multiple sections of the Income Tax Act, 1961, mainly under the Section 194 series.

To make compliance easier, the new law consolidates these provisions into a systematic table under Section 393, which clearly specifies the nature of payment, threshold limit, and applicable TDS rate.

TDS is a mechanism where tax is deducted at the time of making certain payments such as commission, rent, interest, professional fees, or purchase of property. The person making the payment (called the deductor) is responsible for deducting tax and depositing it with the government.

This system ensures regular tax collection, reduces tax evasion, and improves transparency in financial transactions.

Key Payments Covered Under TDS (Payments to Residents)

The Income Tax Act 2025 requires TDS deduction on several types of payments, including:

1. Commission or Brokerage

Payments made as commission or brokerage to agents or intermediaries are subject to TDS.This includes:

- Insurance commission

- Brokerage for sale or purchase of goods

- Commission paid to agents for facilitating business transactions.

2. Rent Payments

TDS applies to rent payments for:

- Land or building

- Plant and machinery

- Furniture and fittings

If the rent amount exceeds the prescribed threshold, the payer must deduct tax before making the payment.

3. Purchase of Immovable Property

When a buyer purchases immovable property exceeding ₹50 lakh, the buyer must deduct 1% TDS before paying the seller.

This provision helps the government track high-value real estate transactions.

4. Interest Income

TDS is applicable on interest income such as:

- Bank fixed deposits

- Post office deposits

- Corporate bonds or securities

However, the law provides higher threshold limits for senior citizens.

5. Contractor Payments

Payments made to contractors for carrying out any work or service are subject to TDS once the payment exceeds the prescribed limit.

6. Professional or Technical Services

TDS must be deducted on payments made for professional services such as:

- Legal services

- Medical services

- Consultancy

- Engineering and technical services

7. Dividend Payments

Domestic companies must deduct TDS before distributing dividends to shareholders once the threshold limit is crossed.

8. E-Commerce Transactions

E-commerce operators are required to deduct TDS when making payments to sellers using their online platforms.

9. Benefits or Perquisites from Business

If a business provides gifts, incentives, or benefits to dealers or distributors, TDS must be deducted if the value exceeds the specified limit.

10. Virtual Digital Assets (Cryptocurrency)

The law also includes provisions for cryptocurrency transactions, where TDS must be deducted on the transfer of virtual digital assets.

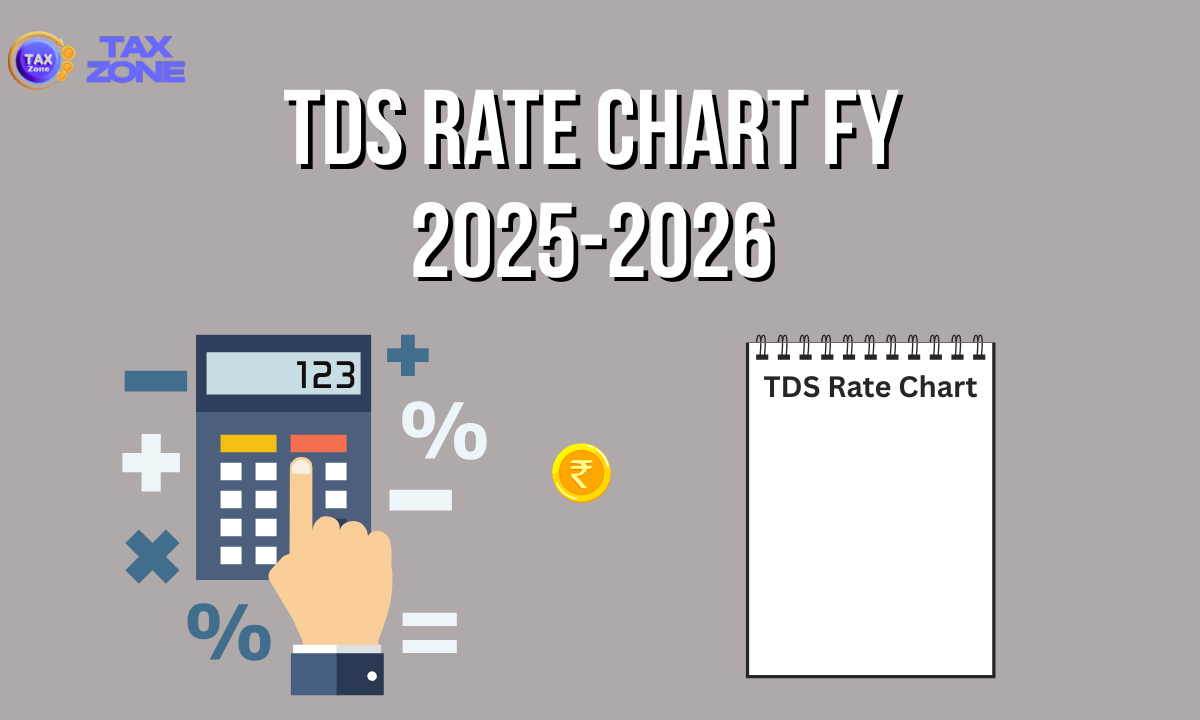

TDS Rate Chart FY 2026-2027 As per Income Tax Act 2025

| Table Sl. No. | New Section (IT Act 2025) | Nature of Payment | Threshold Limit | TDS Rate | Old Income Tax Act Section |

| 1(i) | Sec 393 | Insurance Commission (remuneration for soliciting/procuring business, including renewals) | ₹ 20,000 | Rates in force | 194D |

| 1(ii) | Sec 393 | Commission or Brokerage (other than insurance commission) | ₹ 20,000 | Rates in force | 194H |

| 2(i) | Sec 393 | Rent (Paid by non-specified persons) | ₹ 50,000 per month | 2% | 194-IB |

| 2(ii) | Sec 393 | Rent (a) Plant, machinery, or equipment | ₹ 50,000 per month | 2% | 194-I |

| 2(ii) | Sec 393 | Rent (b) Land, building, furniture, or fittings | ₹ 50,000 per month | 10% | 194-I |

| 3(i) | Sec 393 | Purchase of Immovable Property | ₹50,00,000 | 1% | 194IA |

| 3(ii) | Sec 393 | Certain contractual payments under agreement | Nil | 10% | 194IC |

| 3(iii) | Sec 393 | Compensation on compulsory acquisition of property | ₹5,00,000 | 10% | 194LA |

| 4(i) | Sec 393 | Mutual Fund Units Income | ₹10,000 | 10% | 194K |

| 4(ii) | Sec 393 | Business Trust distributed income | Nil | 10% | 194LBA |

| 4(iii) | Sec 393 | Investment fund income | Nil | 10% | 194LBB |

| 4(iv) | Sec 393 | Securitisation Trust Income | Nil | 10% | 194LBC |

| 5(i) | Sec 393 | Interest on Securities | ₹10,000 | Rates in force | 193 |

| 5(ii) | Sec 393 | Bank / Post Office Interest | ₹50,000 / ₹1,00,000 (Senior Citizen) | 10% | 194A |

| 6(i) | Sec 393 | Payment to Contractor | ₹30,000 single / ₹1,00,000 aggregate | 1% / 2% | 194C |

| 6(ii) | Sec 393 | Work / service payments by Individual or HUF | ₹50 lakh turnover condition | 2% | 194M |

| 6(iii) | Sec 393 | Professional / Technical Services | ₹50,000 | 2% / 10% | 194J |

| 7 | Sec 393 | Dividend Distribution | Nil | 10% | 194 |

| 8(i) | Sec 393 | Life Insurance Policy Payment | ₹1,00,000 | 2% | 194DA |

| 8(ii) | Sec 393 | Purchase of Goods | ₹50,00,000 | 0.10% | 194Q |

| 8(iii) | Sec 393 | Specified Senior Citizen Scheme deduction | As applicable | Rates in force | 194P |

| 8(iv) | Sec 393 | Benefit / Perquisite from Business | ₹20,000 | 10% | 194R |

| 8(v) | Sec 393 | E-commerce transactions | Nil | 0.10% | 194O |

| 8(vi) | Sec 393 | Transfer of Virtual Digital Assets (Crypto) | Nil | 1% | 194S |

Conclusion

The TDS Rate Chart prepared under the Income Tax Act, 2025 serves as a comprehensive guide to the provisions governing Tax Deducted at Source on payments made to residents. By consolidating multiple TDS provisions that were previously spread across various sections of the Income-tax Act, 1961, the new Act presents them in a clear, structured format. This makes it easier for taxpayers, businesses, and professionals to identify the nature of payment, applicable threshold limits, and the corresponding TDS rates.

The chart helps deductors quickly determine when TDS is required to be deducted and at what rate, thereby reducing the chances of errors and non-compliance. It also improves transparency in financial transactions such as commission payments, rent, professional fees, contractor payments, interest income, property transactions, e-commerce payments, and digital asset transfers.

Sources: Income Tax Act 2025

Please read this also: 10 big Changes in New Income Tax Act 2025